Many people delay investing because they feel their principal is small and returns are low. But the true starting point of compounding is not how much you have—it’s when you start and whether you keep contributing.

1. Real numbers first: compounding still creates a gap under low rates

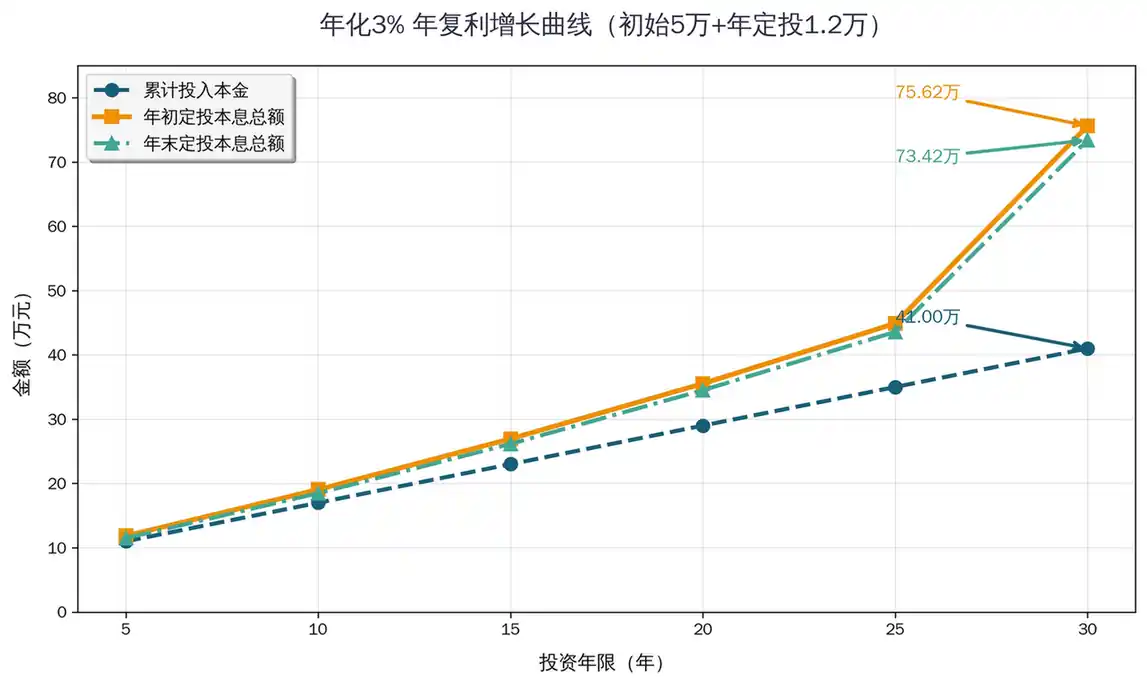

Even with a 3% annual return, long‑term contributions plus compounding can grow wealth far beyond simple saving.

Assumptions that match a typical person’s situation:

- Initial principal: ¥50,000

- Annual contribution: ¥12,000 (about ¥1,000 per month)

- Annual return: 3% (typical low‑risk return)

- Compounding: annual (calculated for contributions made at the start vs. end of each year)

After 30 years:

- Contributions at the start of each year: ¥756,200 total

- Contributions at the end of each year: ¥734,200 total

Your own total contributions are only ¥410,000 (¥50,000 + ¥12,000 × 30). The remaining ¥346,200 (start) / ¥324,200 (end) comes entirely from compounding.

Without compounding (simple interest), the 30‑year total is only ¥532,000, which is more than ¥200,000 less.

That’s the core logic of compounding: even at low returns, time + steady contributions can beat pure saving.

2. A quick visual of low‑rate compounding: slow growth, steady accumulation

Three patterns stand out:

1) First 10 years: returns are tiny, principal matters most

After 10 years you’ve contributed ¥170,000. With contributions at year‑start, the total is ¥190,500, so compounding gains are only ¥20,500—less than 11% of the total.

Compounding is almost invisible here. The main task is simply building principal, and this is the stage where most people give up.

2) Years 20–30: compounding kicks in and gains accelerate

From year 20 to 30, principal grows from ¥290,000 to ¥410,000 (only +¥120,000), but total value jumps from ¥355,400 to ¥756,200. Compounding gains increase from ¥65,400 to ¥346,200.

In the last decade, compounding gains grow more than 5x even at low rates.

3) The longer the time, the higher the gain ratio

After 30 years, compounding gains are nearly 46% of total wealth. That happens with just ¥1,000 per month.

A hard comparison: without DCA, compounding barely matters

If you stop contributions and only compound the initial ¥50,000 at 3% annually, after 30 years you’d have just ¥121,400—over ¥600,000 less than the “initial + DCA” plan.

In a low‑rate world, consistent contributions matter more than compounding alone.

3. How ordinary people can grow steadily in a low‑rate era

3% is already a mainstream low‑risk return today. To make compounding work, you don’t need high yields—just these three habits:

1) Start early: time beats chasing higher returns

In a low‑rate environment, obsessing over a few points of return is pointless. Starting early matters far more.

Even if you begin with ¥10,000 and invest ¥500 per month at 3% annual compounding, after 30 years you could reach ¥358,000.

Start 10 years later with the same contributions and you only reach ¥196,000—a loss of ¥162,000.

The core of compounding in a low‑rate era isn’t “high yield,” it’s “early start.”

2) Choose the right tools: stability first, protect principal

In low‑rate environments, the first principle is stability. Forget high yields; choose tools that preserve principal and let compounding continue without interruption:

- Large‑denomination time deposits (3–5 year terms at major banks)

- Government bonds (fixed coupons, minimal risk)

- Pure bond funds (low volatility, ~2%–3.5% annualized, suitable for DCA)

- Money‑market fund + time deposit combo (cash in MMF, periodically lock into higher‑yield deposits)

The key is to hold long‑term and avoid frequent trading. In low‑rate markets, short‑term moves rarely beat steady compounding.

3) Automate DCA: principal is the base of compounding

With low returns, DCA matters more than yield. A forced ¥1,000 monthly contribution is the core of building principal and enabling compounding.

Set up automatic deductions right after payday. Save first, then spend. Even ¥300–¥500 monthly, done consistently, adds up over time.

Remember: in a low‑rate era, compounding is “small amounts + time.” Small monthly habits become large wealth over decades.

4. Final note: in low‑rate eras, compounding rewards persistence

Many people think 3% compounding “doesn’t matter.” But finance is not about overnight riches—it’s about steady, durable progress.

Thirty years later, when you see ¥750,000 built from a steady ¥1,000 monthly habit, you’ll realize wealth accumulation is simply “save a little each month and let time do the work.”

We can’t change the macro environment. We can change our habits. ¥1,000 a month won’t make you rich overnight, but in 30 years it can fund retirement, education, or an emergency reserve.

Real wealth isn’t created by one lucky bet. It’s created by steady contributions, low‑risk tools, and patience. Start today, keep it simple, and let time surprise you.

Investing involves risks. Be cautious.